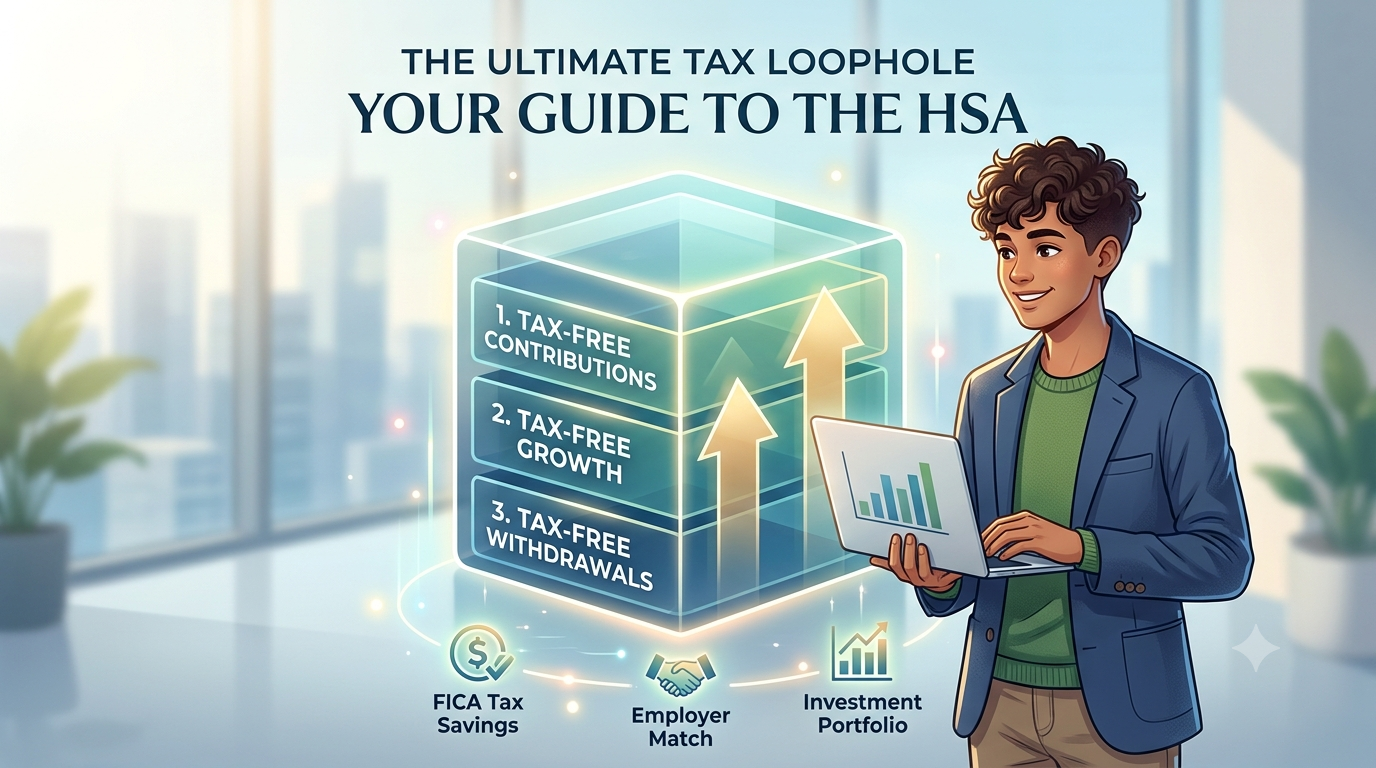

The Ultimate Tax Loophole: A Comprehensive Guide to the HSA (Health Savings Account)

If you are looking for the single most powerful tax-saving and wealth-building vehicle in the United States, look no further than the Health Savings Account (HSA). While many people mistake it for a simple “medical spending bucket,” the HSA actually offers tax advantages and investment flexibility that easily outshine traditional 401(k)s and Roth IRAs.

Let’s dive deep into the five core benefits that make the HSA an absolute “cheat code” for your personal finances.

1. The Unmatched “Triple Tax Advantage”

Under U.S. tax law, almost no other account offers tax-free status at every single stage of your money’s journey. The HSA is uniquely structured with a triple tax advantage:

- Tax-Free Contributions: Any money you contribute to an HSA directly reduces your federal taxable income (pre-tax). Even better, if you contribute through automatic payroll deductions, you completely bypass the 7.65% FICA tax (Social Security and Medicare)—a perk that even standard pre-tax 401(k) contributions cannot claim.

- Tax-Free Growth: Your HSA funds do not have to sit in cash. You can invest them in stocks, mutual funds, or ETFs. Any capital gains, dividends, and interest generated inside the account grow 100% tax-free.

- Tax-Free Withdrawals: As long as you withdraw the money to pay for Qualified Medical Expenses (QMEs), your withdrawals are entirely tax-free, no matter how much your investments have grown.

2. No “Use-It-or-Lose-It” Expiration Dates

People frequently confuse HSAs with FSAs (Flexible Spending Accounts).

- FSAs operate on a strict “use-it-or-lose-it” policy where unspent funds are surrendered to your employer at the end of the year.

- HSAs have no expiration date. The account belongs to you. If you change jobs, get laid off, or retire, the money remains yours forever, continuously compounding in the background.

3. The Pro-Insider Strategy: “Unlimited Deferred Reimbursement”

This is the ultimate wealth-building loophole championed by financial planners:

💡 The “Pay Now, Reimburse Later” Hack

The IRS does not impose a deadline on when you must claim a reimbursement for a medical expense.

- How it works: Suppose you incur $1,000 in medical bills this year. Instead of paying with your HSA card, you pay out-of-pocket using a credit card (earning rewards) and meticulously save the digital receipt.

- The compounding effect: You leave that $1,000 in your HSA to remain invested in the stock market.

- The tax-free payout: 15 or 20 years later, after that $1,000 has compounded and doubled several times over, you can submit your old $1,000 receipt. You can then withdraw $1,000 completely tax-free to use on a vacation, a new car, or daily living expenses.

4. A “Supercharged” Retirement Account After Age 65

What happens if you stay incredibly healthy and accumulate a massive HSA balance by the time you retire?

- Before Age 65: If you withdraw HSA funds for non-medical expenses, you will owe ordinary income tax plus a hefty 20% penalty.

- After Age 65: The 20% penalty is completely waived. If you withdraw money for non-medical reasons, it is treated exactly like a traditional 401(k)—you only pay ordinary income tax.

- The Bonus: You can still withdraw funds tax-free to pay for medical expenses, Medicare premiums, or qualified long-term care insurance. It essentially morphs from a healthcare account into a retirement account with a built-in safety net.

5. Free Money from Your Employer (Employer Match)

To encourage employees to choose High-Deductible Health Plans (HDHPs), many employers will kick in free cash (ranging anywhere from $500 to over $2,000 annually) directly into your HSA. This is free, tax-free money that you can invest immediately.

⚠️ The Golden Rules: Do You Qualify for an HSA?

To legally open and contribute to an HSA, you must meet the following IRS criteria:

- You must be enrolled in a High-Deductible Health Plan (HDHP).

- You cannot have any other “first-dollar” medical coverage (meaning you cannot be covered under a spouse’s traditional PPO plan).

- You cannot be enrolled in Medicare.

- You cannot be claimed as a dependent on someone else’s tax return.

Disclaimer

This guide is for informational and educational purposes only and does not constitute professional financial, tax, or investment advice. Tax laws are complex and subject to change. Please consult with a Certified Financial Planner (CFP) or a Certified Public Accountant (CPA) regarding your specific financial situation before making investment decisions.