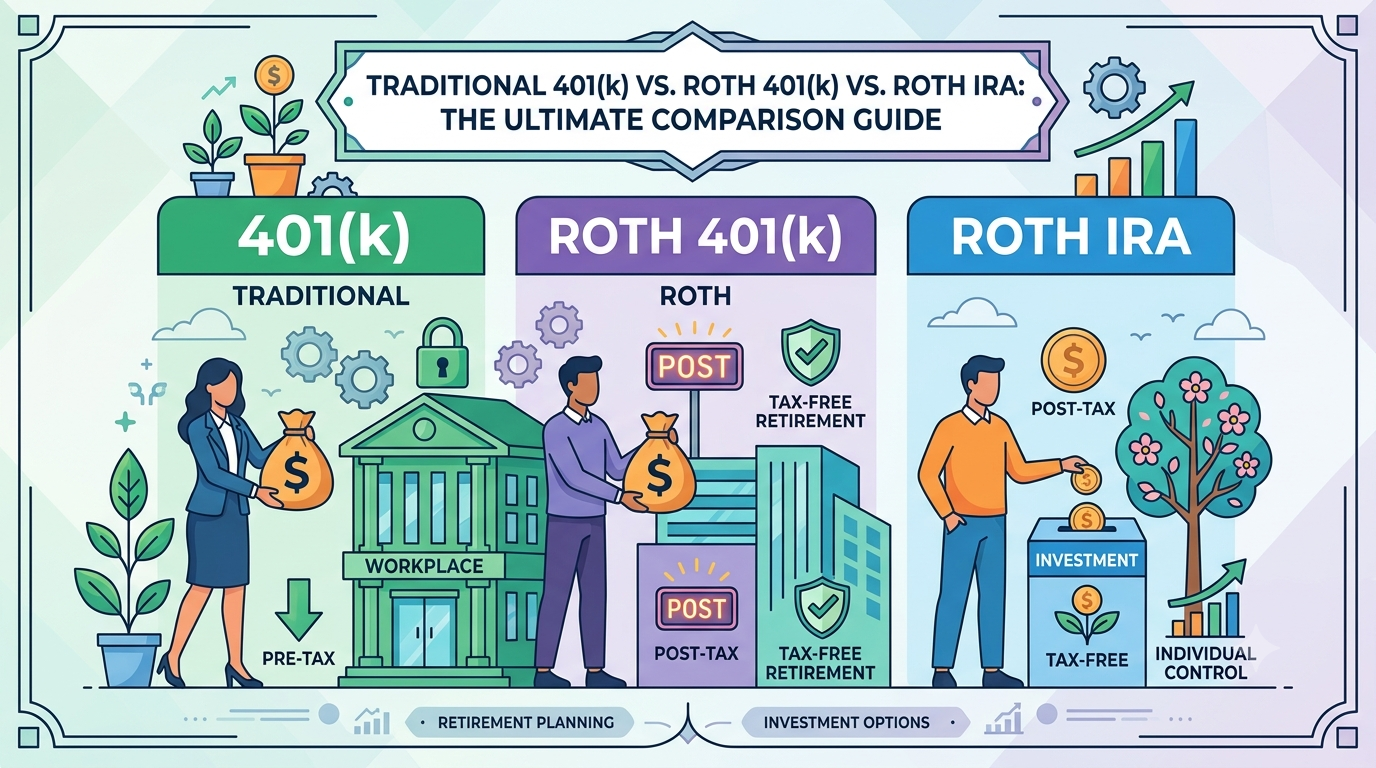

Traditional 401(k) vs. Roth 401(k) vs. Roth IRA: The Ultimate Comparison Guide

Choosing the right retirement account is one of the most impactful financial decisions you can make. The differences between a Traditional 401(k), a Roth 401(k), and a Roth IRA fundamentally come down to three main levers: how they are taxed (now vs. later), how much you can contribute (annual limits), and who controls the account (you vs. your employer).

This guide provides a comprehensive breakdown to help you make an informed decision for your financial future.

1. Quick Comparison Matrix (2026 Tax Year)

| Feature | Traditional 401(k) | Roth 401(k) | Roth IRA |

|---|---|---|---|

| Account Type | Employer-Sponsored | Employer-Sponsored | Individual |

| Tax Treatment | Pre-Tax (Immediate deduction) | Post-Tax (Tax-free withdrawals) | Post-Tax (Tax-free withdrawals) |

| 2026 Contribution Limit | $24,500 | $24,500 | $7,500 |

| Age 50+ Catch-up Limit | +$8,000 | +$8,000 | +$1,100 |

| Employer Match | Yes (Typically pre-tax) | Yes (Typically pre-tax) | No |

| Income Restrictions | None | None | Yes (Phased out for high earners) |

| Required Minimum Distributions (RMDs) | Yes (Starts at age 73) | No (Eliminated starting in 2024) | No (None during your lifetime) |

| Early Withdrawal Flexibility | Stricter (10% penalty + taxes) | Stricter (10% penalty + taxes) | Flexible (Can withdraw contributions anytime) |

Note on Limits: Contribution limits are established by the IRS and are adjusted periodically to account for inflation. The limits shown above reflect the official thresholds for the 2026 tax year.

2. Tax Mechanics: Pay Now or Pay Later?

The core strategy when choosing between traditional (tax-deferred) and Roth (tax-free) vehicles centers on your current tax bracket versus your expected tax bracket in retirement.

Traditional 401(k): Tax-Deferred Growth

- How it works: Your contributions are deducted directly from your gross paycheck before federal and state taxes are calculated. This lowers your Adjusted Gross Income (AGI) for the current year.

- The Trade-off: Your money grows tax-deferred. When you withdraw funds in retirement, both your original contributions and all investment earnings are taxed as ordinary income.

- Best suited for: High earners currently in their peak earning years who expect to be in a lower tax bracket when they retire.

Roth (401(k) & IRA): Tax-Free Growth

- How it works: You make contributions using after-tax dollars. There is no immediate tax deduction, meaning your current-year tax bill remains unchanged.

- The Trade-off: Your investments grow entirely tax-free. When you reach retirement and take qualified withdrawals, you pay $0 in income taxes on both your contributions and your investment growth.

- Best suited for: Investors who are currently in lower or moderate tax brackets, young professionals with decades of compound interest ahead of them, or individuals who want a tax-free “bucket” to hedge against potentially rising future tax rates.

3. Account Logistics: Workplace vs. Individual Plans

While a Roth 401(k) and a Roth IRA share the same tax-free withdrawal structure, their operational mechanics are fundamentally different.

Employer-Sponsored Plans (Traditional & Roth 401(k))

- The Employer Match: This is the single biggest advantage of a workplace plan. If your company offers a matching contribution (e.g., 100% match up to 4% of your salary), this is essentially guaranteed, immediate return on your investment.

- Higher Contribution Ceilings: You can save significantly more in a workplace plan ($24,500 vs. $7,500 in an IRA).

- Curated Investment Menu: You are limited to the fund menu selected by your employer’s plan administrator. These typically include target-date retirement funds, index funds, and select mutual funds.

Individual Retirement Accounts (Roth IRA)

- Complete Investment Freedom: Because you open a Roth IRA individually through a brokerage of your choice, you have access to virtually any listed assetâincluding individual stocks, Exchange-Traded Funds (ETFs), mutual funds, and option strategies.

- Income Eligibility Limits: Unlike 401(k) plans, the IRS restricts who can contribute directly to a Roth IRA. If your modified adjusted gross income (MAGI) exceeds certain annual thresholds, your ability to contribute is phased out or eliminated entirely.

- Tip for High Earners: If you exceed the income limit, you can still fund a Roth IRA utilizing a two-step strategy known as a Backdoor Roth IRA.

4. Withdrawal Rules and Accessing Your Capital

Before locking away your savings, it is crucial to understand when and how you can access your money prior to age 59½.

- Roth IRA (Maximum Flexibility): Because you have already paid taxes on the money you put into a Roth IRA, you can withdraw your personal contributions at any time, for any reason, penalty-free and tax-free. Only the investment earnings are subject to taxes and a 10% penalty if withdrawn early without a qualifying exception.

- Traditional & Roth 401(k) (Stricter Guardrails): Getting money out of an active 401(k) prior to age 59½ is much more difficult. Early withdrawals generally trigger a 10% IRS penalty in addition to ordinary income taxes (unless you qualify for a hardship distribution or opt for a 401(k) loan, which must be repaid).

5. The “Order of Operations” Strategy

If you are trying to figure out how to allocate your savings across these accounts, many financial advisors suggest following this general hierarchy:

- Secure the Match: Contribute to your employer’s 401(k) (Traditional or Roth) up to the exact percentage required to maximize your employer’s matching program. Leaving a match on the table is leaving free money behind.

- Max Out the Roth IRA: Once you have secured your full employer match, direct your next retirement dollars to a Roth IRA to take advantage of low-cost investment options, total portfolio control, and flexible contribution withdrawal rules.

- Return to the 401(k): If you still have retirement funds left to save, return to your workplace 401(k) and continue contributing up to the annual IRS limit.

Disclaimer

This guide is for informational and educational purposes only and does not constitute professional financial, tax, or investment advice. Tax laws are complex and subject to change. Please consult with a Certified Financial Planner (CFP) or a Certified Public Accountant (CPA) regarding your specific financial situation before making investment decisions.