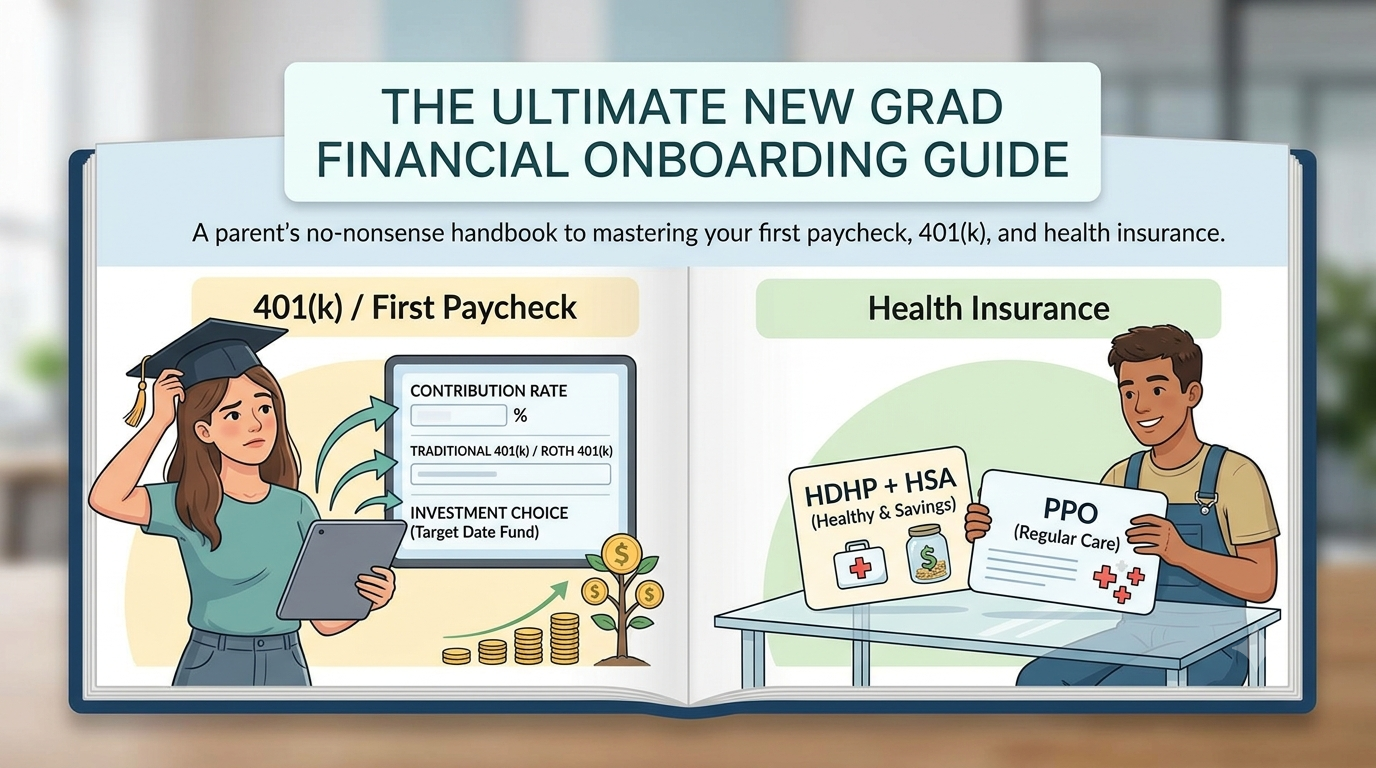

The Ultimate New Grad Financial Onboarding Guide

A parent’s no-nonsense, step-by-step handbook to mastering your first paycheck, 401(k), and health insurance.

Congratulations on your graduation and landing your first job! Walking into the office (or logging in remotely) on Day 1 is an incredibly exciting milestone.

But alongside your laptop, badge, and welcome swag, HR is going to hand you a mountain of paperwork. You will be asked to make critical decisions about your 401(k) retirement account and health insurance that will impact your paycheck and your wealth for years to come.

Don’t panic. You don’t need a finance degree to get this right. This guide translates the confusing corporate jargon into plain English and gives you a step-by-step cheatsheet to optimize your choices from day one.

Part 1: Deciphering Your 401(k) — The Wealth Accelerator

A 401(k) is an employer-sponsored retirement savings plan. HR’s enrollment portal will ask you three fundamental questions: How much to save?, Which tax treatment to choose?, and Where to invest the money?

Step 1: How Much Should I Contribute?

📌 The Golden Rule: Never leave free money on the table.

Most companies offer an employer match. For example, if they offer a “100% match up to 6%,” it means that if you contribute 6% of your paycheck to your 401(k), your company will hand you an additional 6% for free.

- Your Action: Set your contribution rate to at least the minimum percentage required to get the full company match. If the match cap is 6%, your contribution should be at least 6%. Failing to do this is literally throwing away a 100% instant return on your money.

- The Smart Move: If your budget allows, aim for 10% to 15%. You won’t miss the money because you never got used to seeing it in your checking account in the first place.

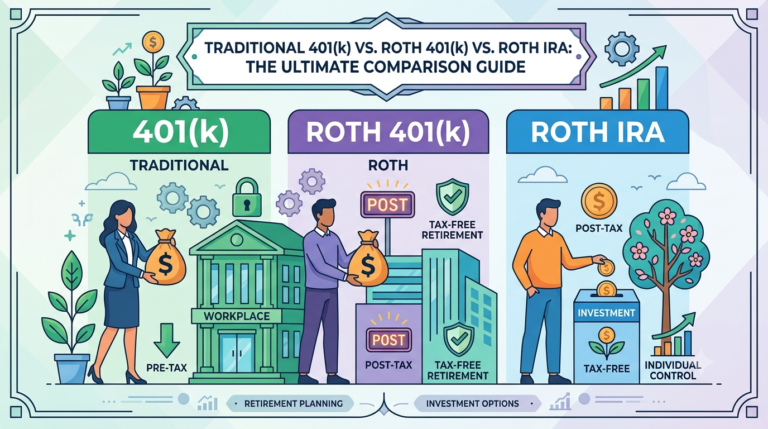

Step 2: Traditional (Pre-Tax) vs. Roth 401(k)

Most modern companies offer two flavors of the 401(k). Here is how to decide which one is right for you:

| Feature | Traditional (Pre-Tax) 401(k) | Roth 401(k) 🌟 (Highly Recommended for New Grads) |

|---|---|---|

| When do you pay tax? | Later. Money goes in tax-free now, but you pay income tax when you withdraw it in retirement. | Now. Money goes in after-tax today, but you pay zero tax when you withdraw it (including all investment growth). |

| Why it fits new grads: | Better if you are currently in your peak earning years and highest tax bracket (not typical for a recent graduate). | Better because you are likely in the lowest tax bracket of your career. Pay the low tax rate now, and let decades of compound growth grow completely tax-free! |

- Verdict: Unless you started your career in an exceptionally high-income tax bracket, choose the Roth 401(k).

Step 3: Where Does My Money Go? (Crucial Step!)

Many people sign up for a 401(k) but forget to choose an investment. If you don’t choose, your money might sit in a “cash/money market” account earning 0% interest. You must invest it.

- Option A: The Set-it-and-Forget-it Option (Target Date Funds – TDF)

- Look for a fund with your estimated retirement year in the name, such as Target Date Fund 2065.

- How it works: It automatically manages your risk. Right now, because you are young, it will invest heavily in high-growth stocks. As you get closer to retirement, it will gradually shift into safer bonds.

- Option B: The Low-Cost Wealth Builder (S&P 500 / Total Stock Market Index Fund)

- If you want to maximize your returns and don’t mind market volatility, find a low-cost stock index fund (look for names like Vanguard, Fidelity, or Schwab index funds with an “expense ratio” lower than 0.05%).

- Young professionals have a 40-year runway—historically, staying 100% in broad-market equities during your 20s yields the highest long-term wealth.

Part 2: Health Insurance — The HSA “Cheat Code”

Health insurance isn’t just about going to the doctor; it is also one of the most powerful tax-shelters in the United States. You will usually have two primary choices: HDHP or PPO.

1. HDHP + HSA (The Ultimate Young Professional Combo)

If you are generally healthy, only see the doctor for your annual physical (which is 100% free under preventive care), and have no expensive daily prescriptions, this is your best choice.

- What is an HDHP? A High Deductible Health Plan has a very low monthly premium (the amount deducted from your paycheck). This means more cash in your pocket every month.

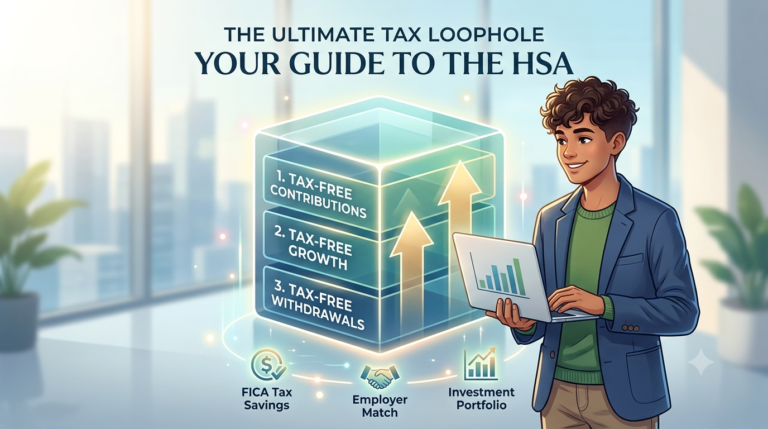

- What is an HSA? A Health Savings Account is a special savings account only available to those on an HDHP. It is widely considered the greatest tax-advantaged account in existence because of its Triple Tax Advantage:

- Tax-Free In: Money you contribute goes in pre-tax, lowering your taxable income.

- Tax-Free Growth: You can invest the money inside your HSA in index funds, and all investment gains grow 100% tax-free.

- Tax-Free Out: You can withdraw the money completely tax-free at any point in your life to pay for medical expenses (including deductibles, dental, vision, prescriptions, and even over-the-counter medicine).

- The “Secret” Perk: Unlike an FSA, HSA money never expires (“use-it-or-lose-it” does not apply). It is yours forever. Plus, many top-tier companies will literally give you free money (seed money) just for opening one—often \$500 to \$1,000 a year!

2. When should you choose a PPO (Preferred Provider Organization)?

Choose a PPO if you manage a chronic illness, see specialists regularly, take expensive brand-name medications, or expect a major medical procedure in the coming year.

- How it works: Your monthly paycheck deductions (premiums) are higher, but your out-of-pocket costs at the doctor are much lower and highly predictable.

💡 The Quick-Start Cheat Sheet

Keep this card handy when clicking through your employer’s portal:

“`text

┌────────────────────────────────────────────────────────┐

│ NEW GRAD DAY-1 CHEATSHEET │

├────────────────────────────────────────────────────────┤

│ [ ] 401(k) Match: Contributing at least _ % │

│ (Check your company policy & match the limit!) │

│ │

│ [ ] 401(k) Type: Choose ROTH 401(k) │

│ │

│ [ ] Investment: Select “Target Date Fund 2065” │

│ or an “S&P 500 Index Fund” │

│ │

│ [ ] Health Plan (Healthy): Choose HDHP + HSA │

│ *Action: Invest your HSA funds! Do not let it │

│ sit as cash. │

│ │

│ [ ] Health Plan (Regular Care): Choose PPO │

└────────────────────────────────────────────────────────┘

Disclaimer

This guide is for informational and educational purposes only and does not constitute professional financial, tax, or investment advice. Tax laws are complex and subject to change. Please consult with a Certified Financial Planner (CFP) or a Certified Public Accountant (CPA) regarding your specific financial situation before making investment decisions.